Crypto markets have historically been led by retail investors, with professional investors following. Is that changing? After all, high-tech innovation in the past 15 years has executed an opposite about-face, flipping an enterprise-led pattern into a consumer-led pattern.

Retail’s lead was evident in the fourth quarter of 2017, as media hype soared, alongside the price. There’s no doubt the retail hype is quieter this time around. CNBC had nearly 100 “bitcoin” headlines in the first half of Q4 2017. These past six weeks, as bitcoin ran to a new all-time high in market value, it’s put up less than 40. Where the hell are Davy Day Trader and the “Robinhood effect” investors? Did their stimulus checks run out?

It’s premature to diagnose a secular trend in crypto investing, mostly because the retail/institutional dichotomy is problematically simplistic. Below, I’ll run through four dimensions of the market that show how the participants in this run-up are behaving differently than investors did in 2017:

- Bitcoin whales and trading vs. holding

- Bitcoin vs. ether and everything else

- Regulated vs. off-shore futures markets

- N. America vs. E. Asia investors

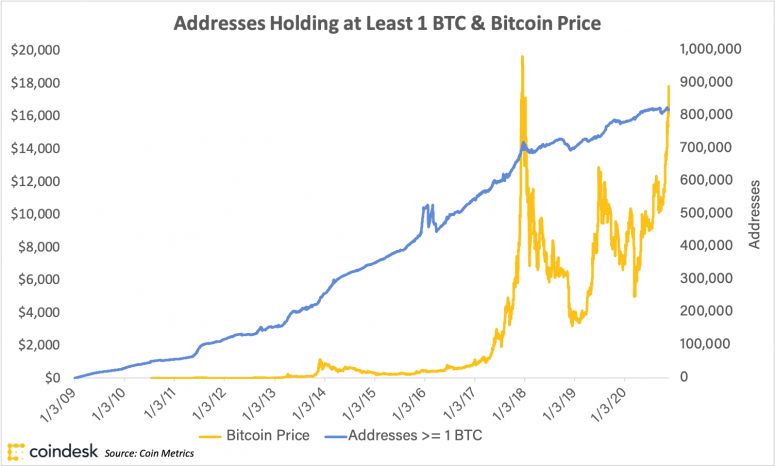

1. Bitcoin whales and trading vs. holding

The number of addresses holding at least 1 bitcoin increased at an unrelenting pace from the end of 2013 to the 2018 crash. It picked up again in 2019, then leveled off again this spring. This is different from the end of 2017, when it soared to a peak with the bitcoin price.

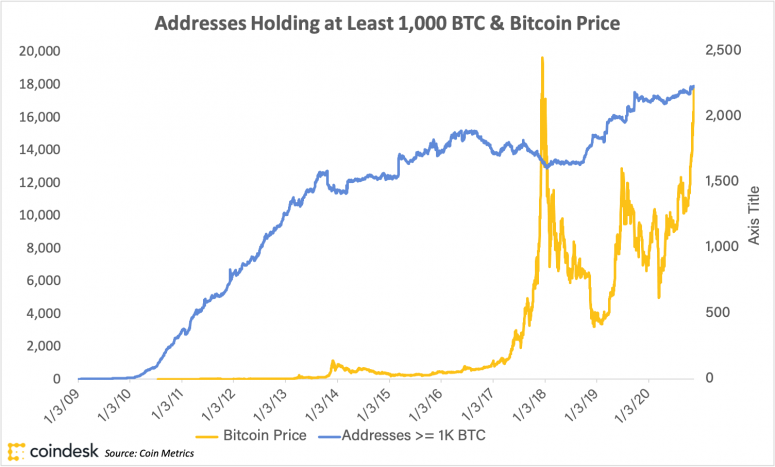

Compare that to the number of what we could call bitcoin “billionaires,” addresses holding at least 1,000 BTC. These whales were selling into the run-up in 2017. This time, the Bitcoin blockchain’s Forbes List is growing, not shrinking.

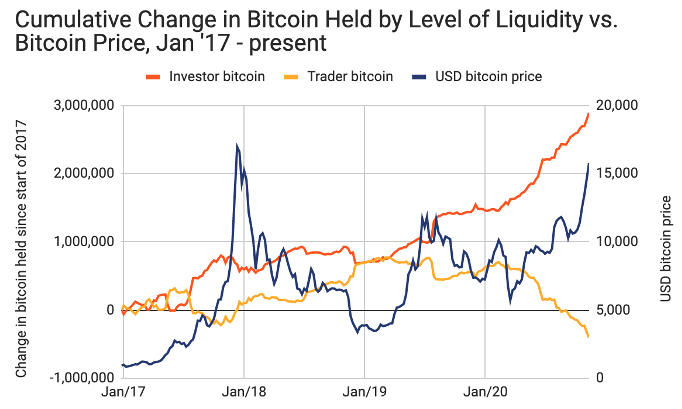

Address balances must be taken with a grain of salt; addresses ≠ entities. Behavior is a better signal. If there be whales, where are they swimming to? Wherever they winter, they are bringing their bitcoin bags along. The orange coin is accumulating more in wallets that historically buy and hold, and less in wallets that have shown a tendency to trade.

Twice since 2017, a slowing in holder accumulation has been a leading indicator for the market top. In 2020, it shows no sign of slowing, yet.

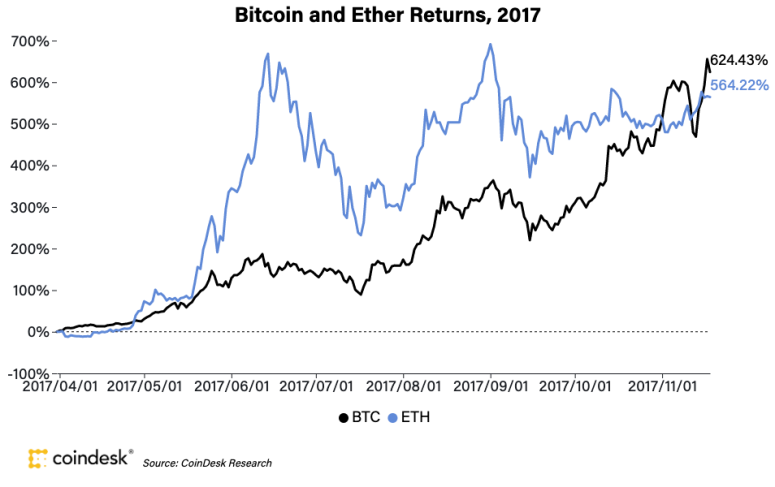

2. Bitcoin vs. ether and everything else

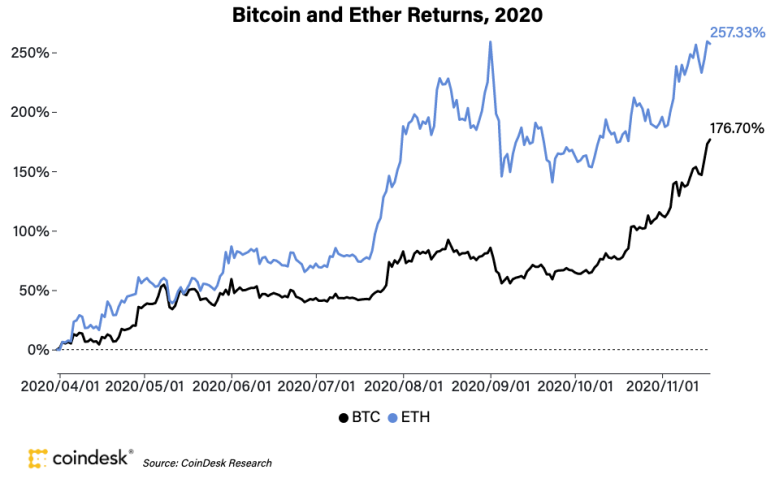

The 2017 bull market is remembered as a phenomenon driven by enthusiasm for initial coin offerings (ICOs) on Ethereum. However, by the time the frenzy reached its fever pitch, ether (ETH) had largely completed its run. At the midpoint of 2017 Q4, bitcoin returns were 23.9%; ether returns were 6.9%. It was bitcoin’s Q4 catch-up run that fed the bulls.

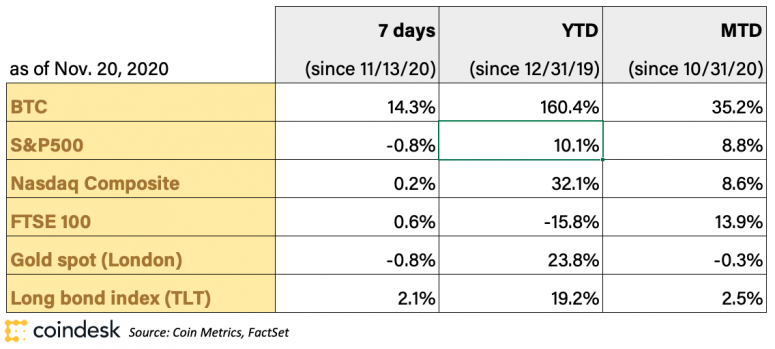

Contrast that to 2020, and the similarities and differences are telling. Again, ether led the run-up, but this time it’s keeping pace with bitcoin, returning 23.2% so far on the fourth quarter to bitcoin’s 28.4%, even before it crossed $500, early Friday. If 2017’s pattern repeats, the bitcoin bulls may have a longer range to run.

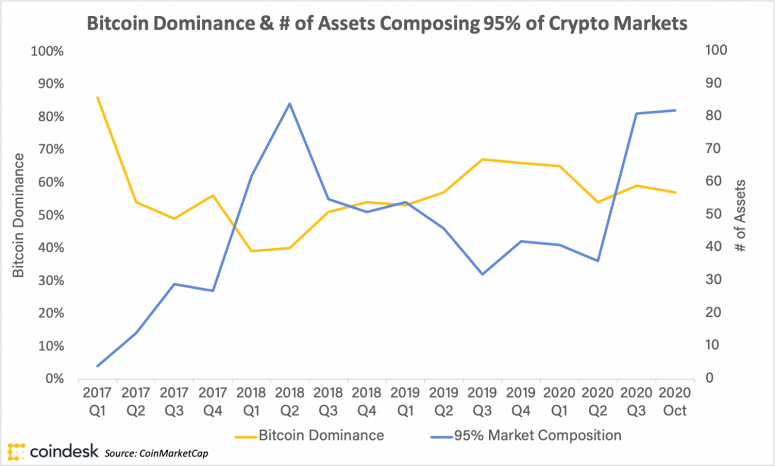

So, are crypto markets consolidating? The answer is, yes and no. Bitcoin dominance, the orange coin’s share of cumulative market cap, is in the high 50s. Usually, that means a shorter list of assets that compose the bulk of the market. Not this year.

Top-five assets in the CoinDesk 20 are growing with bitcoin, but the long tail is now more fragmented than it has been since the aftermath of the 2017 bubble. (This tally includes stablecoins and other pegged assets.)

3. Regulated vs. off-shore futures markets

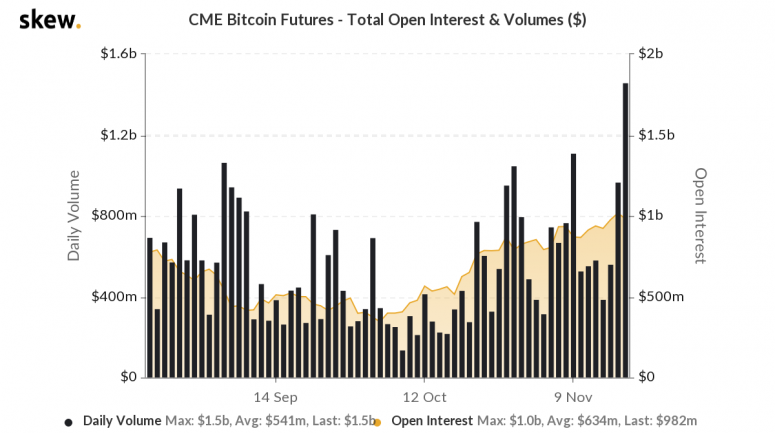

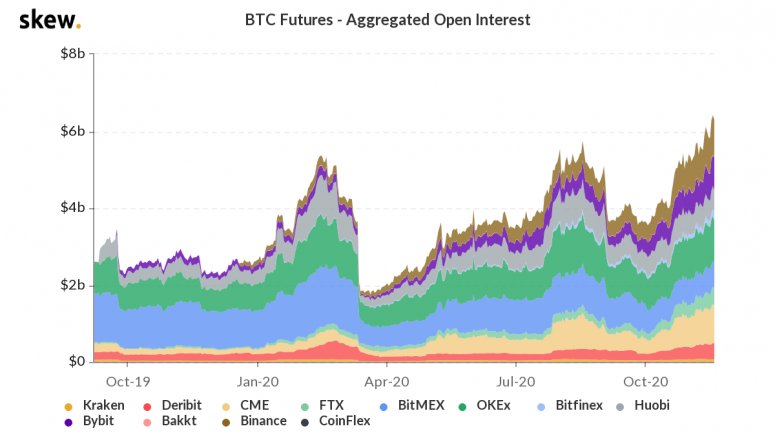

The “institutions are here” chorus can sing about the growth of the CME Bitcoin Futures market, signaling increasing demand for regulated exposure to bitcoin via established operations channels. Open interest on the CME hit $1 billion this week, an all-time high.

However, much of that growth is attributable to bitcoin’s price run. And in aggregate, lightly regulated derivatives contracts, traded by individuals, prop desks and liquidity providers, dwarf the CME. It would be unwise to base an institutional flippening thesis on growth in the CME alone. Better to say institutional participation is growing with the rest of the market.

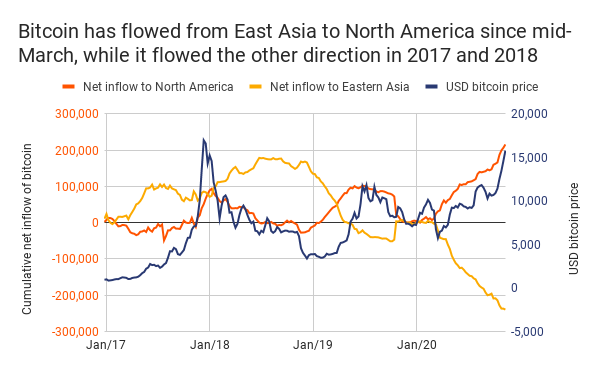

4. N. America vs. E. Asia investors

Parallel to the growth of CME futures is the flow of bitcoin onto North American exchanges, and off of East Asian exchanges.

To the extent exchange flows represent the activity of participants, East Asian investors have been selling bitcoin into this bull market at rates never before seen. Meanwhile, North American interest in bitcoin is greater than it was in 2017.

One important caveat: the flows here may represent the preferences of traders more than the long-term activity of investors. The stablecoin tether is on pace to grow its market cap by more than $10 billion this quarter. Some of the flows in East Asia likely represent Tether’s (USDT) march toward quote currency dominance, as traders increasingly favor it over bitcoin in crypto-to-crypto markets.

Conclusion

The takeaway: This bull run is indeed different from 2017, though that doesn’t mean we won’t see another peak-and-trough cycle. Signals that hint at the kinds of investors who are participating indicate we may be earlier in the cycle than we were when bitcoin hit its all-time high three years ago. Bitcoin’s history is full of narratives about upcoming shifts or regulatory change s that would change the market fundamentally. Those narratives have been overblown in the past, and they’re probably overblown now. The same is true of narratives that foretell the dollar’s demise.

Are traditional financial markets burning down their own frat house? Maybe, but that doesn’t suddenly transform bitcoin into a safe haven or a hedge. The current patterns of new, larger and longer-term investors’ growing involvement is likely to continue, but bitcoin and downmarket cryptos will be risk-on investments for the foreseeable future, and investors should continue to treat them as such.

Anyone know what’s going on yet?

One of the things that makes bitcoin such a successful investment is its lack of infrastructure. Like most retail investors, I tend to take profits too early. Like many bitcoin investors, I keep my coins in cold storage, which means it takes time and effort to get them ready to trade. We bitcoin investors are akin to the apocryphal Fidelity clients, who died and, in death, stopped mucking around with their portfolios, thereby becoming more successful than other Fidelity customers.

That said, bitcoin’s returns this month have put the orange coin into a stratospheric percentage of my family’s portfolio. Anyone else out there getting white knuckles, yet?

(Note: Nothing in this newsletter is investment advice. The author owns some bitcoin and ether.)

CHAIN LINKS

Rick Rieder, CIO of fixed income at BlackRock, is thinking about crypto assets. In case you’ve been living under a rock, yourself, Rieder made comments on CNBC Friday morning that indicate the world’s largest asset manager is taking crypto seriously: “Do I think it’s a durable mechanism that … could take the place of gold to a large extent? Yeah, I do, because it’s so much more functional than passing a bar of gold around,” Rieder said. TAKEAWAY: If BlackRock walks the walk Rieder is talking, we all better put on our running shoes to keep up.

IBM has secured a patent covering blockchain-based transactions in massively multiplayer online video games like Fortnite and Call of Duty: Warzone. TAKEAWAY: Blockchain startups in the game industry have touted similar technology as a way to secure player ownership of virtual goods and their portability between games, but it’s unclear whether existing incentives in game development and publishing would support moving to such a structure. It’s doubly unclear how permissioned blockchains like the kind IBM has championed would improve upon a simple database in these cases.

One potentially overlooked factor in the current bitcoin run-up: Beijing’s crackdown on over-the-counter crypto trading desks, where miners convert new-minted bitcoin into cash. We broke it down in a new CoinDesk partnership with Axios, this week (check it out), after reporting the news on Monday. TAKEAWAY: The 2020 Bitcoin Halving reduced the impact of new supply on the market. With more investors holding, demand factors may be more of a driver in this run-up. This is more a medium-term supply issue to monitor, as it may shape the makeup of bitcoin mining.

Brian Brooks, a former Coinbase general counsel, has gotten a White House nod to serve a five-year term to lead the Office of the Comptroller of the Currency, the primary U.S. bank regulator. Brooks, who has been serving as Acting Comptroller, has already overseen a public letter allowing nationally regulated banks to offer crypto custody and to handle accounts for stablecoin issuers. TAKEAWAY: Most of the air in crypto goes to securities- and commodities-markets regulators. For the non-regulated currencies that top the CoinDesk 20 list of crypto assets, bank regulation may be more significant as an enabler of infrastructure that professional investors need, in order to participate.

Offshore crypto exchange operator Binance has sued Forbes and two of its journalists alleging defamation over a story on the so-called “Tai Chi” documents, reportedly leaked from inside Binance, detailing a strategy for regulatory misdirection in the U.S. TAKEAWAY: CEO Changpeng “CZ” Zhao has been coy about his company’s corporate structure, refusing to say where Binance’s jurisdictional headquarters lie. It’s a sign of crypto infrastructure’s immaturity when one of the largest exchange operators won’t tell you what law they operate under.

Goldman Sachs expects the digital yuan, China’s planned national virtual currency, to reach 1.6 trillion rmb ($229 billion) in issuance and 19 trillion rmb ($2.7 trillion) in annual total payment value within 10 years. TAKEAWAY: If you think PayPal’s move to embrace bitcoin is exciting as an onramp to crypto, you should be frenzied over the opportunity presented by central bank digital currencies (CBDCs). Their aptitude as a gateway drug depends heavily on structure and regulation, but the potential is there.

In Japan, 30 firms have announced a collaborative effort to issue a private digital yen and Mitsubishi UFJ Financial Group (MUFG), one of Japan’s largest banks, has announced plans to launch a blockchain payment network in 2021. TAKEAWAY: This looks quite different from China’s digital yuan (see above), but both are examples of ways in which digital currencies can reach mainstream banking and its customers. East Asian economies are ahead of the U.S. and Europe in this. If you think U.S. and EU adoption of this kind of technology seems far-fetched, please reflect that you probably said the same thing about text messaging in 2005.

Podcast episodes worth listening to

Source