While many U.S. crypto exchanges are using the latest bull run to spruce themselves up in hopes of impressing institutional investors and regulators, China’s so-called “Big Three” centralized crypto exchanges (CEX) – Binance, Huobi and OKEx – are slinging mud at each other.

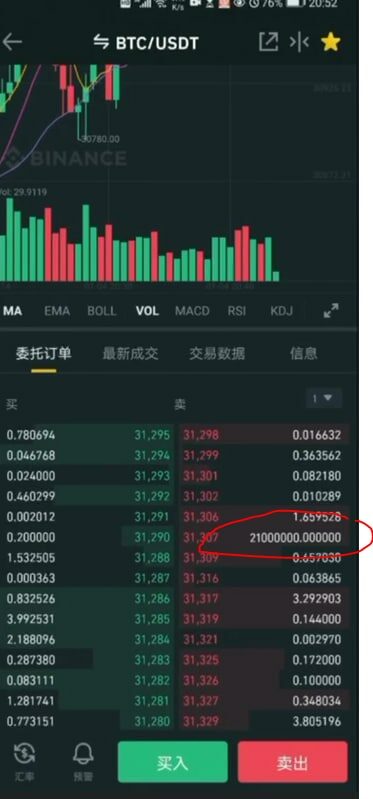

The latest flap is over a bogus video that purports to show a single sell order of 21 million bitcoin on Binance on Jan. 4. The clip went viral last week on WeChat, a popular China-based social media platform.

The video, viewed by CoinDesk, claims that bitcoin’s price took a hit after the order was completed. Screenshots in a WeChat group’s chats show that some users appear to be furious, accusing Binance of “market manipulation.”

The angry reactions ignored the fact that the 21 million number alludes to the total amount of bitcoin that will ever be mined, sometime by the year 2140 (bitcoin’s total supply currently stands at 18.6 million). So clearly 21 million bitcoin could not have been sold. Besides, most major exchanges’ bitcoin reserve data are available to trace.

But because we’re nothing if not thorough, CoinDesk confirmed with several on-chain data firms, including CipherTrace and CryptoQuant, that no orders of that size were placed on Binance at the time the video purports to show.

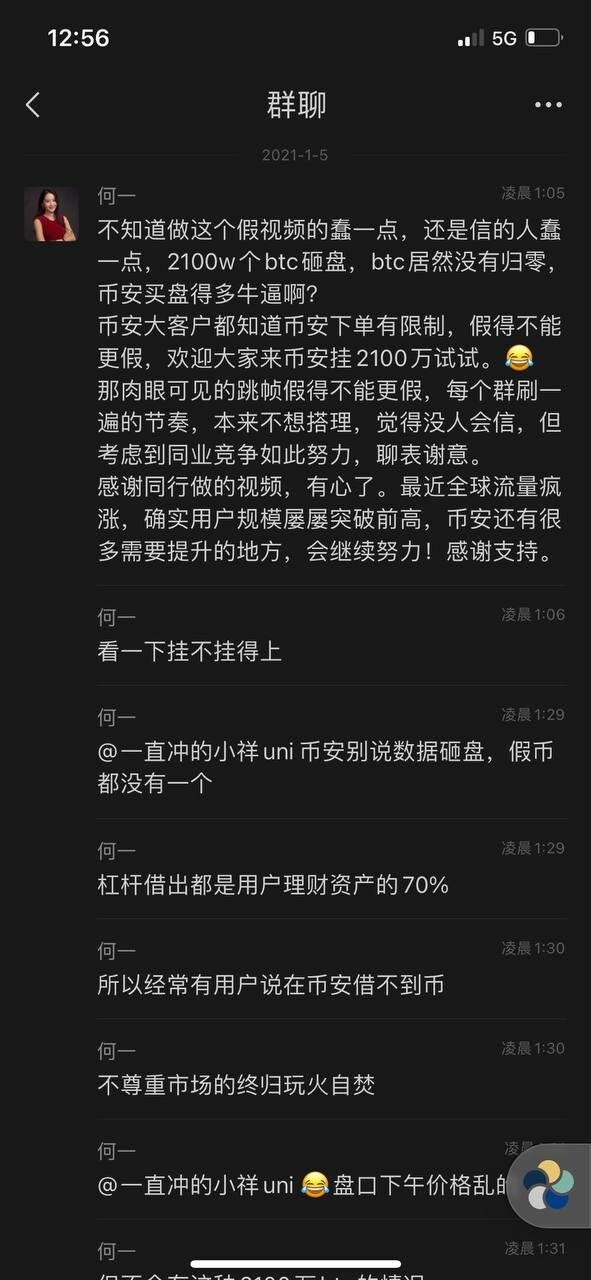

A Binance executive spoke out about the video on WeChat, throwing shade at unnamed “competitors” he claimed were behind the video.

The video “could not be more fake,” Yi He, co-founder and chief marketing officer of Binance, wrote in Chinese on WeChat. “I was not going to respond because I thought nobody was going to believe it, but considering how ‘hard-working’ our competitors were to post it on every group chat, I just wanted to express my appreciation.”

As of press time, Binance did not respond to CoinDesk’s requests for comment.

If you looked at English-language social media platforms, you would think the three China-originated centralized crypto exchanges coexist in peace and harmony. But a survey of Chinese-language platforms reveal a differing dynamic. Screenshots of chats and public posts on WeChat and other popular Chinese social media platforms such as Weibo show multiple disputes among the three exchanges over the past several years. This is not the first time Binance’s He has confronted executives from rivals OKEx and Huobi on social media.

He’s accusations notwithstanding, both Huobi and OKEx denied responsibility for the latest incident. Ciara Sun, vice president of global business at Huobi Group, denied Huobi was involved in “the creation of the video,” and told CoinDesk the video “falsely” recorded a sell order on Binance’s platform.

“As a global financial organization that adheres to both ethical and regulatory standards, we value honesty and transparency within our organization and do not rely on misleading marketing tactics that would erode the trust of our community,” Sun said.

Likewise, OKEx CEO Jay Hao told CoinDesk that crypto exchanges are often the victims of false accusations of “price manipulation.”

“Anyone with knowledge of this industry would immediately be able to dismiss a photo like this, but it’s unfortunate that some investors still suffer from these types of groundless and fictitious accusations,” Hao said.

It’s not just business, it’s personal

Normal business competition, centered on capturing market share in China, is only one part of the tensions involving the three exchanges. These hard feelings go back at least four years, when OKCoin’s then-CTO, Changpeng Zhao, and co-founder Yi He left what was at the time the largest Chinese crypto-to-fiat exchange to start Binance, according to Colin Wu, a China-based crypto writer who previously worked in the country’s crypto mining industry.

Meanwhile, OKCoin, along with other China-based bitcoin trading platforms, closed their trading operations in the country and moved offshore after Chinese regulators banned initial coin offerings in late 2017. OKEx has worked as a separate entity from its parent company OK Group or OKCoin since 2017, a spokesperson told CoinDesk previously. OKCoin now is a San Francisco-based crypto exchange, led by Chief Executive Hong Fang.

Huobi joined the fray slightly later and friction among the three exchanges really intensified after each launched crypto derivatives products. OKEx currently is the second-biggest derivatives exchange by bitcoin open interest, followed by Binance and Huobi. (The CME is the largest thanks to growing interest from institutional investors in the U.S.)

Several sources, who agreed to speak on the subject anonymously due to close business relationships with the three exchanges, told CoinDesk that as the competition heats up again there may be an uptick in tricks and false information such as the fake Binance video. In turn it can cause a lot of “fear, uncertainty and doubt” (FUD) among retail traders and investors in China, especially those who are relatively new to the market.

“The video came out at a time when retail sentiment was at the peak,” one source said. “When people are scared of the top, they could be easily aroused by anything like this.”

“No matter how much the cryptocurrency space has matured, there will always be interested parties from without who leap at the chance to cause FUD amongst traders,” OKEx’s Hao said.

Source