Today’s most successful entrepreneurs tapped into their wealth through startup technology companies such as Amazon, Oracle, Facebook and Microsoft. Just ask Jeff Bezos, Larry Ellison, Mark Zuckerberg and Bill Gates, who continue to serve as the world’s tech leaders.

Yet, the stage is still open for additional leaders to join this round table of sorts, and the invitation is floating throughout the blockchain and cryptocurrency space. With leaders such as Binance’s Changpeng Zhao and Ethereum’s Vitalik Buterin, many cryptocurrency companies today are still hoping to capture the Silicon Valley promise: aiming to shift away from centralized businesses and transform existing infrastructures into a decentralized ecosystem while recognizing that traditional Wall Street ventures such as Goldman Sachs have still not felt the need to penetrate this industry.

As the wealth continues to spread across many throughout the industry, the new crypto vogue-rich such as CZ aren’t yet sitting at the same table of net worth as Facebook’s Mark Zuckerberg, who has continued to be in the privacy hot seat in recent years — but they are catching up quickly.

The overall growth and “success” that companies such as Uber enjoyed early on can now be traced back to the participation of its earliest adopters, simply through supply and demand subsidies.

Why reinvent the wheel?

Ridesharing platforms such as Uber and Lyft connect people who need immediate transportation with system-vetted drivers that can provide such a service. The same goes for Airbnb, which connects individuals who need a place to stay with those who choose to offer their furnished homes for short-term rentals. There’s an extremely high demand for rentals surrounding global tech conferences, including but not limited to Las Vegas’ Consumer Electronics Show, Austin’s South by Southwest, Utah’s Sundance Film Festival and the World Economic Forum, for example.

Indeed, looking to two Silicon Valley-based startups such as Uber and Airbnb with users on both the supply and demand sides of these networks only brings home the fact that the blockchain and crypto spaces don’t need to reinvent the wheel or come up with a new growth model. It’s already there.

When Uber first launched, it was faced with the dilemma of choosing which pool of customers to focus on first — the supply side or the demand side — to effectively grow its user base. According to a recent Harvard Business Review case study on Uber, Etsy and Airbnb, these companies focused on a two-tiered growth phase.

The classic phases of growth

The first step was getting the first 1,000 users by focusing on the service side of the equation. In the case of Uber, it focused on offering incentives to black-car drivers.

Uber went on to the second tier of the growth phase where it was focused on the customer side for rideshare users from 1,001 to 1,000,000. The case study mentioned above went on to identify that in their growth phases, Uber and Airbnb reduced costs for a competitive advantage. After that, these companies moved on to the third phase — the extraction phase — by increasing prices.

Airbnb’s founders, Brian Chesky and Joe Gebbia, used a more traditional means of marketing by creating a great incentive program for hosts, which also emphasizes how Uber launched in situations of high demand and low supply, rolling out one city at a time.

For example, after Uber got its first 1,000 drivers, it focused on giving away cash to riders who got their friends to download and use the app, with a $20 coupon for a free ride that users could share as a gift with their friends.

To achieve the most out of a growth phase, companies typically raise large capital rounds from financial institutions to fund their initial growth by subsidizing the product and service costs to make them unfairly cheap compared with other services. As a result of growth incentive mechanisms for bootstrapping, the startup’s network effect grows out and users come pouring in. But the economic model has to be done just right, especially when there are double-sided networks as there are with companies such as Uber and Airbnb on the supplier and customer sides.

Uber has raised an estimated $24.7 billion United States dollars to successfully launch and grow the business to where it is today. With an in-app incentive-aligned mechanism, Uber from the very beginning designed a way to circumvent the competitive barrier to entry dilemma. In fact, it’s this incentive-based economic model and theory that Uber raised money on. Its investors expected it to burn the money into the Uber community through incentives because they believed in how Uber used subsidies in its incentive-aligned mechanism and the network effect from popular demand.

Network effect economics

After a few months of using Uber, early adopters began to grow dependent upon ridesharing and crave the “addiction” that it offered. This was evident when the company reached 1 million users, where Uber entered into the next phase of the incentive-aligned mechanism, centered around so-called “network effect economics.” Recognizing that dependence, Uber increased its prices, allowing the company to make back the money it spent on growth.

What followed was extraction, which Harvard Business Review recognizes as a typical high-level startup to an initial-public-offering economic model, based on an incentive growth strategy.

Token economics

The most successful growth models that crypto projects such as Bitcoin (BTC) utilize have strong similarities in their economic incentive models to that of traditional Silicon Valley startups.

Bitcoin’s two-sided model, or token economics, consists of those that spend to make transactions and the miners that provide computing resources to ensure they are done correctly. Coined back in 2017, “token economics,” or cryptoeconomics, was used to describe the economic incentive design thinking behind decentralized protocols and applications.

It was under this concept that Bitcoin succeeded where other early decentralized protocols failed. It succeeded not because of proof-of-work, the idea of decentralized cash or even fault-tolerant consensus but because it incorporated this idea of cryptoeconomics at the core of its consensus protocol.

If we were to accept the premise that Satoshi Nakamoto invented Bitcoin in 2009 to be, at its earliest stages, an inflationary currency — where at every four years, inflation would decrease until it reaches zero — it could be argued that what Nakamoto actually envisioned was a mirror image of Uber’s economic model. Under this belief, could it be that Nakamoto actually “growth-hacked” their way to success?

Peer-to-peer networks to today

The value of a peer-to-peer network grows by the number of participants squared, according to Metcalfe’s Law. If there are five people on Facebook, the value is 25 because five people can talk to one another 25 ways. If there are 1 million people on Facebook then the network effect is 1 trillion. Therefore, P2P networks are worth their value in users squared.

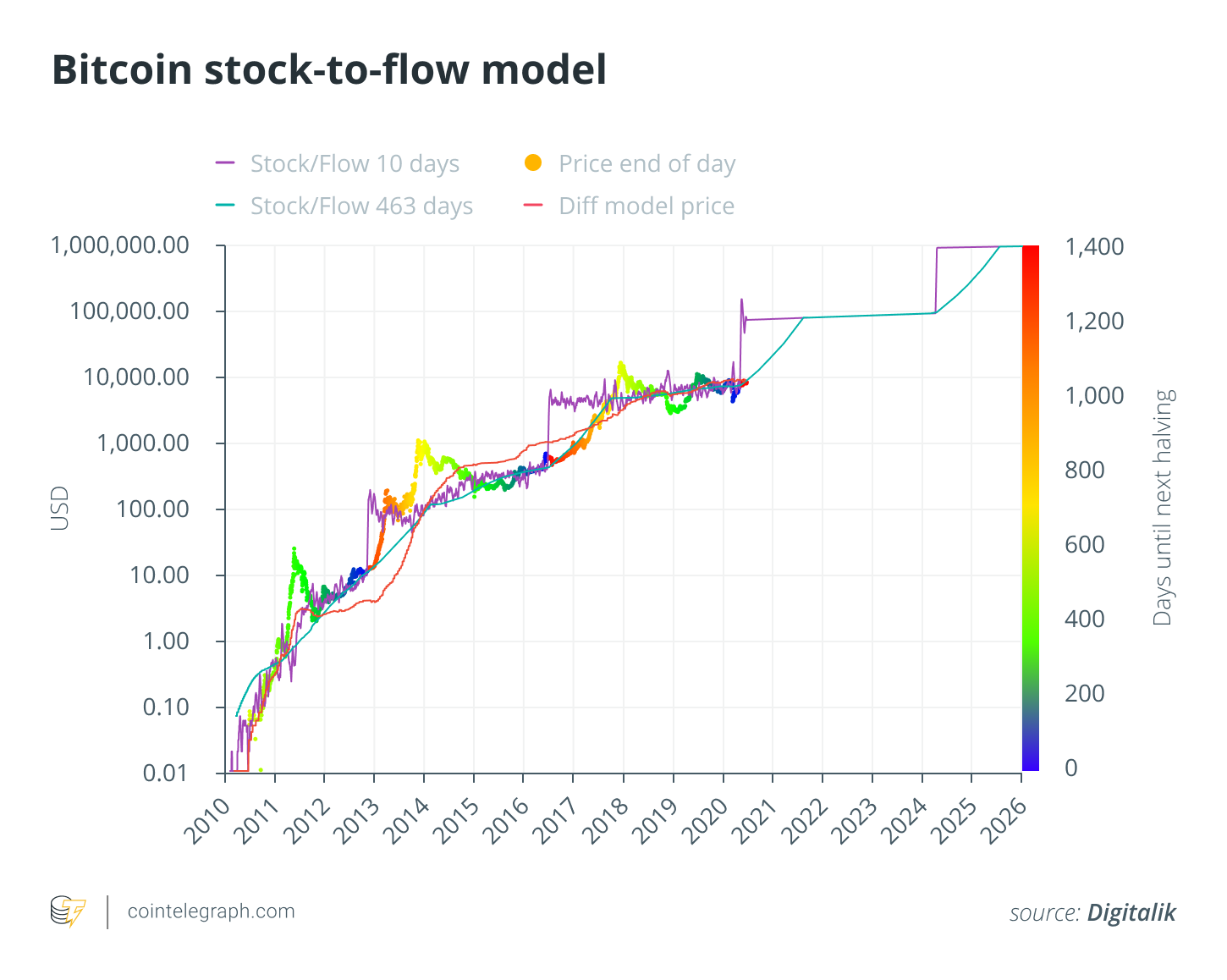

Bitcoin has a stock-to-flow ratio similar to precious metals such as gold. Stock is the amount of gold, and flow is the production of it — the mining block rewards — and it’s measured over the course of one year. Gold has the highest stock-to-flow ratio in the sense that on an annual basis, you can only ever mine a tiny amount of new gold relative to all the gold on the planet. That’s why it’s more stable. When you look at stock-to-flow ratio charts for Bitcoin, it looks like a curve that grows upward but eventually rounds off at the top.

In the chart above, you can see that from 2010 to 2011, the stock to flow ratio of Bitcoin was less than 200, which means there was 200 BTC in existence for every 1 BTC newly mined. Today, it’s 1,000 BTC for every 1 BTC newly mined. In the future, there will be even less BTC newly mined, following the next halving date.

Mechanism design

Block rewards were really important in Bitcoin’s early stages because they incentivized the community to perform the actions that the system requires: to produce the currency itself. The monetary inflation provided early participants with the ability to earn Bitcoin for performing an important mining task at a time when Bitcoin had a low value. Miners were incentivized by combining their efforts with reasonable hope that their Bitcoin mined in 2011 had the potential to increase in value in the future. This created enough of an incentive to attract miners, holders and supporters of the early Bitcoin network.

While the Bitcoin network does in fact experience inflation, the inflation rate gradually declines over time until it asymptotically reaches zero. However, Bitcoin wouldn’t be where it is today if Nakamoto hadn’t incorporated a cryptoeconomic model at the core of its consensus protocol with the goal to extrapolate the network effect by embedding incentive-aligned mechanisms into everything including transitions, computation, storage, prediction and power.

Blockchains enable us to enforce scarcity and facilitate value transfer in otherwise impossible situations, enabling society to expand the range of problems where economic incentive models can be successfully applied. Human behavior, though difficult to predict, can be very predictable when the right incentives are applied to trigger the behaviors necessary to take a blockchain to mass adoption. That’s what happened in the case of Bitcoin miners.

Early Bitcoin mining had a low barrier to entry because all you had to do was install a miner on your laptop to start earning freshly minted Bitcoin for what you mined. Mining back then was a lot like minting is today. Miners provide security, an important feature of the system, and are rewarded for their efforts.

Over the years, decentralized finance — which generally refers to the digital assets and financial smart contracts, protocols and decentralized applications, or DApps, built on Ethereum — has become a rapidly growing niche within the cryptocurrency industry where we are witnessing networks successfully apply new innovative incentive models.

Back in May, Cointelegraph spoke with the CEOs of DeFi companies Compound Finance and Kava Labs regarding their experiences with dForce and the key takeaways the hack could bring the DeFi community.

In Cointelegraph’s conversation with Brian Kerr, the CEO of lending platform Kava Labs, he shared his thoughts on the viability of the Ethereum network as it currently stands. In its current form, according to Kerr, Ethereum’s architecture doesn’t meet the scaling and security needs of the DeFi sector, as the level of testing required to achieve all outcomes is infinite in the Solidity programming language. The CEO concluded that he believes it is for these reasons and many others that leading projects including Binance, Cosmos and Kava have chosen to leave the Ethereum ecosystem for greener pastures.

For those unfamiliar with Kava, the DeFi lending platform enables loan generation to users of major cryptocurrencies and is frequently described as the “Uber of Bitcoin.” In recent years, Kerr and his team have adopted the growth-by-decentralization model by automating the process for users anywhere in the world to instantly generate loans and seamlessly connect them to global demand — think of a global marketplace where you can exchange your loans for dollars, euros, Chinese yuans, etc. If our financial lenders ever think to bring student loans into this ecosystem, we could see a massive change in how loans are utilized and paid back over a period of time — but that’s a conversation for another time.

So, how does Kerr’s view toward Ethereum’s viability fit into the idea of having an “Uber-like” growth model that borrows characteristics from a traditional P2P marketplace?

In a follow up to Cointelegraph’s previous conversation in May, he explained that “growing a decentralized network requires both the supply and demand side, which are robust and have incentives.” He added:

“Decentralized systems, like any P2P marketplace need participants and a healthy amount of capital to get off the ground. It’s not enough to build a decentralized business; you have to inject a sizable amount of cash into the system to start the ‘network effect snowball’. No matter the market dynamics — be it one-sided or two-sided, the piece needed to ignite a network effect, is often first subsidies in the form of cash rewards or credits.”

Interestingly enough, Binance’s CZ quickly jumped into our conversation, ahead of the lending platform’s announcement that it would be supporting the upgrade of the Kava mainnet ecosystem. As CZ shared with us via email:

“The Kava community is providing KAVA rewards to the initial users that stake BNB, enabling BNB users to take part in the on-chain governance on the proof-of-stake based Kava platform.”

“This is a really exciting time for BNB holders,” said CZ, adding that Kava “is a pretty well incentive-aligned mechanism for bootstrapping USDX liquidity, which is incredibly important for the early stages of creating a new stablecoin. Great to see that Kava is not only building upon the shoulders of giants, like MakerDao, but also advancing innovation and bringing to the table new mechanism design ideas.”

The views, thoughts and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.

Andrew Rossow is a millennial attorney, law professor, entrepreneur, writer and speaker on privacy, cybersecurity, AI, AR/VR, blockchain and digital currencies. He has written for many outlets and contributed to cybersecurity and technology publications. Utilizing his millennial background to its fullest potential, Rossow provides a well-rounded perspective on social media crime, technology and privacy implications.

Source